simple vs compound interest: the 6% monthly trading rule explained

most traders think doubling their account is impossible. they hear "100% annual returns" and immediately assume it's reserved for hedge fund managers or incredibly lucky traders.

but here's what they're missing: the difference between simple vs compound interest changes everything.

when you understand how compound interest works in your trading account, that "impossible" 100% return becomes a tangible 6% per month. same destination. completely different mental load.

let me show you the math that changes how you think about account growth.

table of contents

- the difference between simple vs compound interest

- how compound interest works in trading accounts

- the actual math: monthly returns compounded over 12 months

- breaking down impossible goals into achievable targets

- is 6% monthly actually realistic?

- advantages retail traders have over institutions

- mindset shifts: from home runs to base hits

- key takeaways

- frequently asked questions

the difference between simple vs compound interest

before we dive into trading applications, let's clarify what simple vs compound interest actually means.

simple interest calculates returns only on your original principal. if you make 6% per month with simple interest, you'd calculate:

- 6% × 12 months = 72% annually

- on a $10,000 account, that's $7,200 in gains

compound interest calculates returns on your growing balance. each month's gain becomes part of next month's principal. with compound interest:

- 6% per month = 101.22% annually

- on a $10,000 account, that's $10,122 in gains

the difference?

$2,922 in extra returns purely from compounding.

and that's the power most traders completely overlook when setting account growth goals.

how compound interest works in trading accounts

here's where it gets interesting for traders...

I've talked to thousands of traders who think doubling their account is unrealistic. "100% annual returns? that's not possible."

but when you understand simple vs compound interest, you realize:

100% per year = 6% per month (compounded)

same goal. completely different feeling.

when you frame it as "I need 100% returns this year," your brain shuts down. it sounds insurmountable.

but when you reframe it as "I need to average 6% per month," suddenly it becomes tangible.

the key difference is understanding that compound interest means your monthly targets grow with your account. you're not just making 6% on your original $10,000 each month. you're making 6% on your new balance, which includes all previous gains.

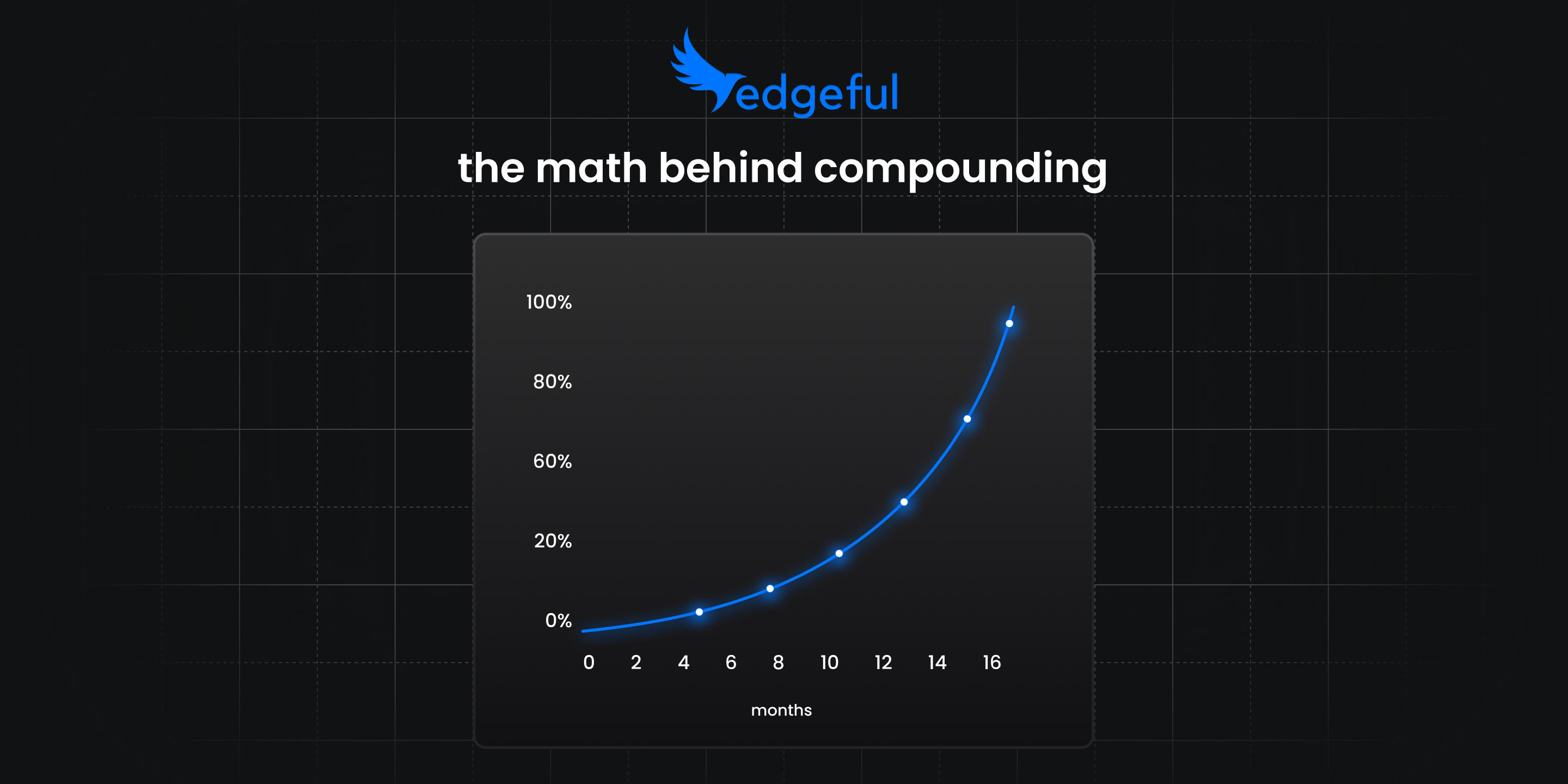

the actual math: monthly returns compounded over 12 months

let's break down exactly what happens when you apply compound interest to different monthly return targets over a full year.

here's what compounding does to monthly returns over 12 months:

- 1% per month = 12.68% annually (not 12%)

- 2% per month = 26.82% annually (not 24%)

- 3% per month = 42.58% annually (not 36%)

- 4% per month = 60.10% annually (not 48%)

- 5% per month = 79.59% annually (not 60%)

- 6% per month = 101.22% annually (not 72%)

at 6% monthly, compound interest adds an extra 29.22% to your annual returns compared to simple interest.

that's nearly a third of your total gain coming purely from the compounding effect.

this is the mathematical reality of simple vs compound interest in action. most traders mentally calculate using simple interest (just adding up monthly percentages), but your actual account grows using compound interest principles.

breaking down impossible goals into achievable targets

so what does 6% per month actually look like when you break it down further?

6% per month equals:

- ~1.5% per week

- ~0.3% per trading day (assuming 20 trading days per month)

making 0.3% on your account in a single day doesn't sound impossible, does it?

that's the point.

when you stop thinking about the annual goal and start focusing on the daily or weekly targets... the "impossible" becomes manageable.

let me show you what this looks like in practice with compound interest working for you...

if you start with $10,000:

- month 1: hit $10,600 (6% = $600)

- month 2: hit $11,236 (6% = $636)

- month 3: hit $11,910 (6% = $674)

- month 6: hit $14,185

- month 12: hit $20,122

you just doubled your account.

notice how your monthly dollar targets get bigger as your account grows? that's compound interest at work. you're always making 6% of your current balance, not your starting balance.

manageable. measurable. repeatable.

is 6% monthly actually realistic?

okay, so the math works. but can you actually achieve these compound interest gains consistently?

two things make this achievable:

1) data-backed strategies work

when you're trading with proven edge — real historical data showing probabilities, customizations for what days of the week to trade, and key levels to set stops and take profits at — you're not gambling.

you're executing a process.

the traders who blow up aren't using strategies grounded in data. they're trading on feelings, hunches, and hope.

but when you know your strategy has a proven track record over hundreds of trades... you're not guessing. you're implementing a system with tangible, real edge.

this is how compound interest becomes achievable rather than theoretical. consistent edge, applied repeatedly, compounding over time.

2) retail traders have advantages institutions don't

here's something most traders don't realize...

retail traders actually have advantages when it comes to hitting these compound interest targets:

- size: you're not moving millions of dollars. you can get in and out of positions without significant slippage.

- speed: you're not waiting for committee approvals. you can adapt to market conditions in real time.

- flexibility: you're not bound by mandates or style boxes. if a strategy stops working, you stop trading it.

institutions may have capital, but retail traders have agility. and when you're targeting 6% monthly gains through compound interest, agility matters more than capital.

mindset shifts: from home runs to base hits

here's what separates consistent traders who benefit from compound interest from everyone else...

they're not swinging for home runs.

every trader I've worked with who blows up is doing the same thing: trying to 10x their account in a week. they're looking for the one trade that changes everything, so they take outsized risk when they don't need to.

and they blow up. every time.

the traders who double their accounts year after year through compound interest aren't making 50% on single trades.

they're making 1-3% on dozens of trades. small, consistent wins. compounded over time.

understanding simple vs compound interest changes your entire approach. you stop chasing massive single-trade gains and start stacking incremental edge.

let compound interest do the heavy lifting. trust the process, not the outcome of any single trade.

how edgeful helps you execute this compound interest strategy

at edgeful, we've built the platform specifically to help you trade with data-backed edge that supports consistent compound interest growth:

100+ reports: see exactly how your strategy has performed historically. no guessing. just data going back 5 years.

what's in play: know which setups are most likely to trigger today, in real time, so you can focus on high-probability trades.

customizable filters: tailor reports to your trading style — day trading, swing trading, specific tickers, specific market conditions.

when you're trading with this level of data backing your decisions... 6% per month stops feeling like a stretch goal.

it starts feeling like a baseline for compound interest growth.

frequently asked questions

what is the difference between simple and compound interest?

simple interest calculates returns only on your original principal, while compound interest calculates returns on your growing balance. in trading, if you make 6% monthly, simple interest would give you 72% annually (6% × 12), but compound interest gives you 101.22% annually because each month's gains become part of next month's principal.

how does compound interest work in a trading account?

compound interest in trading means your returns are calculated on your current account balance, not your starting balance. if you start with $10,000 and make 6% in month one, you earn $600. in month two, you make 6% on $10,600 (your new balance), earning $636. this compounding effect continues, turning 6% monthly into 101.22% annually instead of just 72%.

is 6% monthly return realistic for traders?

yes, 6% monthly returns are achievable with data-backed strategies and consistent execution. when broken down, 6% monthly equals approximately 1.5% weekly or 0.3% per trading day. retail traders have advantages like size, speed, and flexibility that make these compound interest targets realistic when trading with proven edge rather than emotions.

how much can I make with compound interest in trading?

with 6% monthly returns and compound interest, a $10,000 account grows to $20,122 in 12 months (101.22% gain). the compound interest effect adds an extra $2,922 compared to simple interest calculations. over time, compound interest growth accelerates as your account balance increases.

why do most traders fail to achieve compound interest growth?

most traders fail because they swing for home runs instead of consistent base hits. they try to 10x their account quickly rather than targeting manageable daily or weekly gains. successful traders who achieve compound interest growth make 1-3% on dozens of trades, letting the compounding effect do the heavy lifting over time.

key takeaways

here's what you need to remember about simple vs compound interest in trading:

- compound interest calculates returns on your growing balance, not just your original principal

- 6% monthly with compound interest = 101.22% annually (not 72% with simple interest)

- compound interest adds +29.22% annually at 6% monthly returns

- 6% per month = ~1.5% per week = ~0.3% per day

- data-backed strategies make consistent compound interest growth achievable

- retail traders have advantages institutions don't (size, speed, flexibility)

- stop swinging for home runs. stack base hits. let compound interest work.

the next time someone says doubling your account is unrealistic... show them the math on simple vs compound interest.

p.s. if you're struggling to grasp futures trading, we've got you covered with our new futures trading free course. by signing up, you'll get sent 5 lessons via email, covering multiple topics to help you unlock the required skills to becoming a profitable trader.