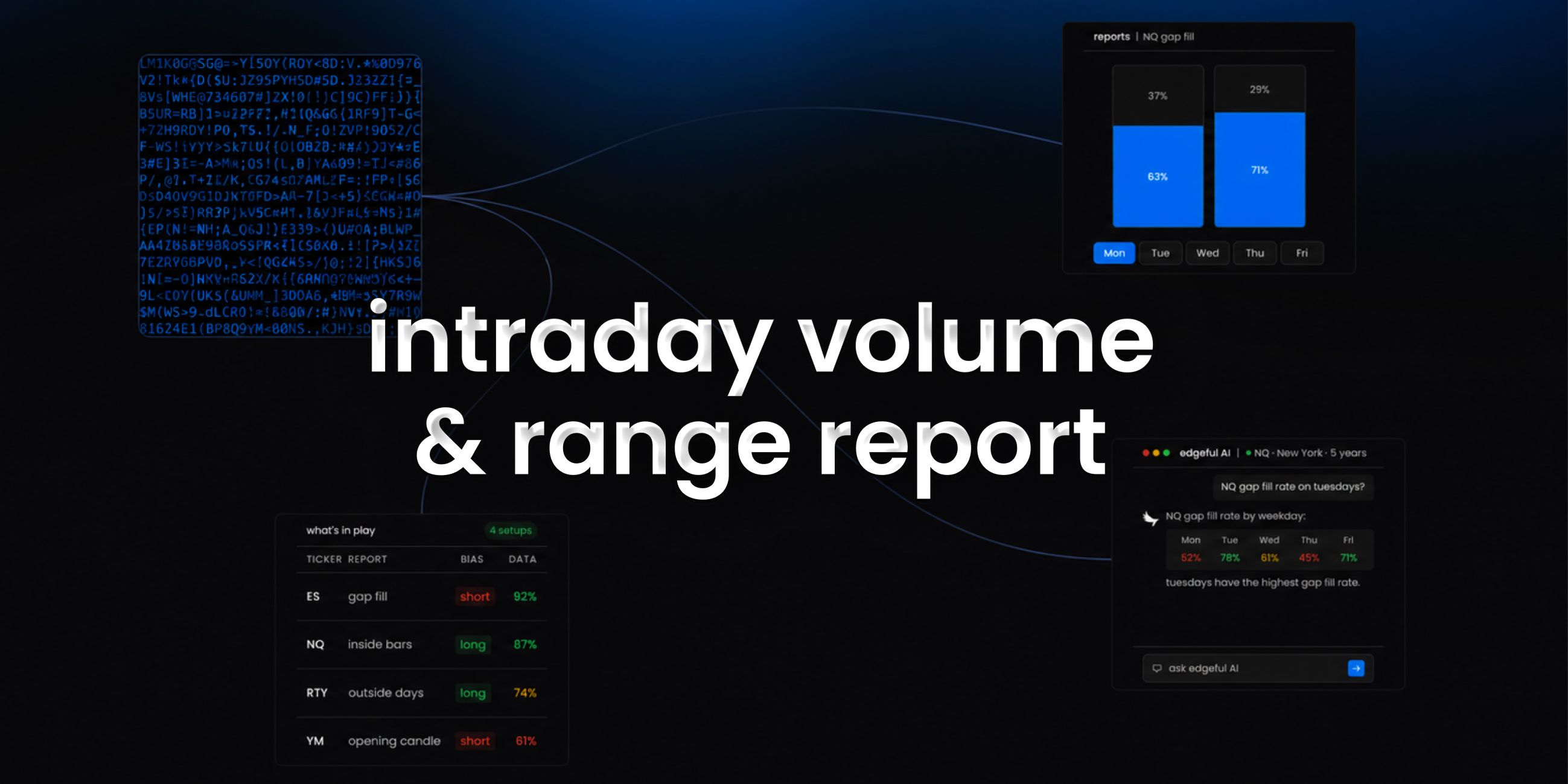

intraday volume and range report: what it measures and how traders use it

the intraday volume and range report on edgeful analyzes how average volume and average price range move through the trading day.

tracks volume and range bucketed by time interval so you can see exactly when the session is most active and when it dies into chop.

this is one of the 150+ reports available on the edgeful platform. here's how it works, what the data shows, and how traders use it.

table of contents

- what the intraday volume and range report measures

- how the calculation works

- available subreports

- how traders use intraday volume and range data

- combining intraday volume and range with other reports

- key takeaways

what the intraday volume and range report measures

aggregates historical intraday data into time buckets and shows three numbers for each bucket — average volume, average absolute range (high minus low), and average percentage range. surfaces when the session is most active versus when it goes quiet.

the report is available for futures, stocks, ETFs, forex, and crypto. you can filter by ticker, session (NY, London, Asian, full globex, or custom), timeframe (5m, 15m, 30m), and lookback period.

how the calculation works

the intraday volume and range report groups historical data by time of day and aggregates.

- the report extracts the time component from every candle in the lookback

- it calculates absolute range (high minus low) and percentage range (range divided by low, times 100) for each candle

- volumes, ranges, and percentage ranges are averaged across all instances of each time bucket

- overnight sessions use special chronological sorting so the time series reads correctly

- the result is a time-of-day profile of volume and volatility

available subreports

the intraday volume and range report has 1 subreport for deeper analysis:

by weekday. groups the same volume and range buckets by weekday. surfaces whether specific days of the week have unique intraday profiles — useful for traders who only trade certain days or want to scale into the most active windows.

how traders use intraday volume and range data

- identifying the high-momentum windows in your session so you can attack when conditions favor follow-through

- cutting yourself off once volume historically dies — protecting yourself from low-quality chop trades

- sizing position around the time of day with the most range

- pairing with intraday timing to confirm both volume and timing align with your setup

- building data-backed session rules instead of trading every minute of the day the same way

the data doesn't tell you to trade. the intraday volume and range report tells you the historical performance of the setup in front of you. what you do with that information is your decision.

results require customization, time, and effort. the numbers change depending on your ticker, session, and lookback period. always check the data for your specific conditions.

combining intraday volume and range with other reports

the intraday volume and range report works best when combined with other edgeful reports for confluence:

- use the what's in play dashboard to see intraday volume and range data alongside your other favorite reports in one view

- the screener lets you scan up to 49 tickers for intraday volume and range setups across 4 reports simultaneously

- edgeful AI can analyze intraday volume and range data alongside other reports and find patterns you'd never spot manually

key takeaways

- the edgeful intraday volume and range report measures average volume and average range bucketed by time of day

- available for futures, stocks, ETFs, forex, and crypto with full session, ticker, timeframe, and date range filtering

- 1 subreport available: by weekday

- part of the 150+ reports included in the edgeful essential plan ($49/month or $39/month annual)

- works best when combined with other reports using what's in play, the screener, or edgeful AI

trading involves risk. past performance and historical data do not guarantee future results. the statistics referenced in this post are based on historical data and may not reflect future market conditions. always trade with proper risk management.